What Do Homebuyers Need to Know Before Escrow Begins?

What Do Homebuyers Need to Know Before Escrow Begins?

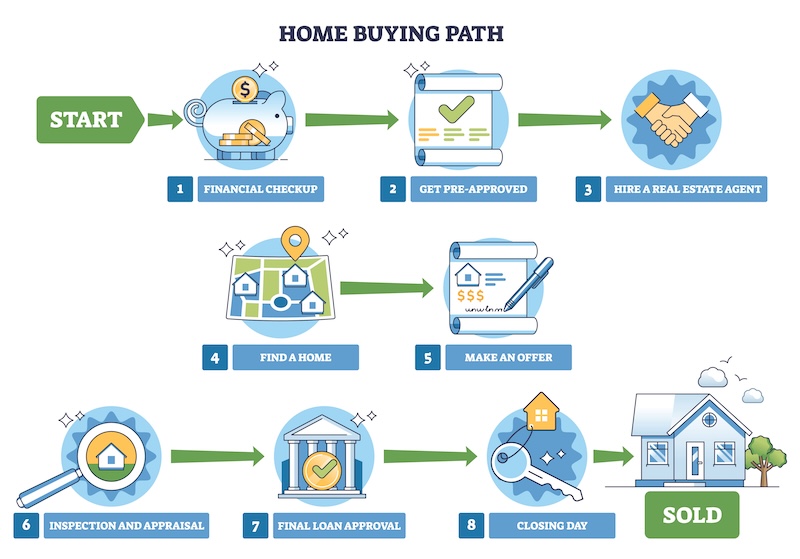

As the Southern California real estate market continues gaining momentum during the spring and summer buying season, many buyers start searching for homes before fully understanding the financing process. That excitement often leads to confusion surrounding two very common mortgage terms: pre-qualification and pre-approval. Although many people use those terms interchangeably, they represent very different stages in the home-buying process. Understanding the distinction helps buyers prepare more effectively, make stronger offers, and move through escrow with fewer surprises.

At the same time, escrow plays a critical role once a seller accepts an offer. Escrow helps coordinate communication, documentation, timelines, and financial transactions between all parties involved. Buyers who understand how financing and escrow work together often experience a much smoother transaction overall.

What Pre-Qualification Actually Means

Pre-qualification usually serves as the earliest step in the mortgage process. During pre-qualification, a lender reviews basic financial information provided verbally or through a simple online application.

That information may include:

- Estimated income

- Approximate debt levels

- Credit score range

- Employment details

- Estimated down payment

- General financial background

Based on that information, the lender provides an estimate regarding how much the buyer may qualify to borrow. Pre-qualification offers buyers a rough idea of their purchasing power, but it does not involve deep financial verification. In many cases, lenders do not fully review tax returns, pay stubs, bank statements, or supporting documentation during this stage. Because of that, pre-qualification carries less weight in a competitive real estate market.

Why Pre-Approval Carries More Strength

Why Pre-Approval Carries More Strength

Pre-approval involves a much more detailed review of the buyer’s finances. Instead of relying primarily on self-reported information, lenders verify documentation directly.

That process commonly includes reviewing:

- W-2s

- Tax returns

- Pay stubs

- Bank statements

- Credit reports

- Employment history

- Debt obligations

- Asset documentation

Once the lender completes that review, the buyer receives a formal pre-approval letter outlining the loan amount for which they qualify. Sellers and real estate agents typically view pre-approved buyers much more favorably because the lender has already verified the buyer’s financial position. In competitive markets, pre-approval often strengthens an offer significantly.

Why Sellers Prefer Pre-Approved Buyers

From a seller’s perspective, financing uncertainty creates risk. A buyer who only completed pre-qualification may still face substantial hurdles once the lender begins fully reviewing financial documents. That uncertainty can delay escrow or even cause transactions to collapse. Pre-approved buyers generally present lower risk because the lender already completed much of the financial verification process. Although final underwriting still occurs later, pre-approval provides stronger evidence that financing will likely move forward successfully. That distinction matters tremendously when multiple buyers compete for the same property.

From a seller’s perspective, financing uncertainty creates risk. A buyer who only completed pre-qualification may still face substantial hurdles once the lender begins fully reviewing financial documents. That uncertainty can delay escrow or even cause transactions to collapse. Pre-approved buyers generally present lower risk because the lender already completed much of the financial verification process. Although final underwriting still occurs later, pre-approval provides stronger evidence that financing will likely move forward successfully. That distinction matters tremendously when multiple buyers compete for the same property.

How Escrow Fits Into the Home Buying Process

Once a seller accepts an offer, escrow officially begins. Escrow acts as a neutral third party responsible for managing the transaction and helping ensure that all contractual obligations are completed properly before funds and property ownership transfer.

The escrow company helps coordinate:

- Earnest money deposits

- Contract documentation

- Title review

- Loan payoff information

- Buyer and seller instructions

- Contingency timelines

- Final signing appointments

- Distribution of funds

- Recording of ownership documents

Escrow essentially serves as the organizational hub of the real estate transaction.

Without escrow, buyers and sellers would face much greater risks involving funds, documentation, and legal compliance.

Why Financing Delays Impact Escrow

Why Financing Delays Impact Escrow

Financing remains one of the biggest factors affecting escrow timelines. If buyers enter escrow without strong financial preparation, problems may surface later during underwriting. Missing documentation, undisclosed debt, credit issues, employment changes, or insufficient reserves can delay loan approval significantly. Those delays often create stress for everyone involved. Buyers who obtain full pre-approval before shopping for homes usually move through escrow more efficiently because much of the lender’s verification work already occurred upfront. That preparation helps reduce surprises later in the transaction.

The Importance of Earnest Money Deposits

Once escrow opens, buyers typically submit an earnest money deposit. That deposit demonstrates serious intent to purchase the property. Escrow securely holds those funds while the transaction progresses. The escrow company helps ensure that funds remain protected and properly distributed according to the purchase agreement. Buyers gain confidence knowing their funds stay managed by a neutral third party rather than transferring directly to the seller. That structure helps protect both buyers and sellers throughout the process.

Escrow Coordinates Communication Between Multiple Parties

Real estate transactions involve many moving parts and multiple professionals working simultaneously.

Those parties may include:

- Buyers

- Sellers

- Real estate agents

- Mortgage lenders

- Title companies

- Home inspectors

- Insurance providers

- Contractors

- County recording offices

Escrow helps coordinate communication among all parties while tracking deadlines and required documentation. Strong escrow coordination often helps transactions stay organized and on schedule even when unexpected issues arise.

Why Buyers Should Avoid Major Financial Changes During Escrow

One common mistake buyers make involves changing their financial situation after pre-approval and during escrow.

For example, buyers sometimes:

- Open new credit cards

- Finance vehicles

- Change jobs

- Make large purchases

- Miss payments

- Transfer large sums between accounts

Those changes can create problems during final loan underwriting. Even buyers who already received pre-approval may encounter financing complications if their financial profile changes significantly before closing. Escrow officers and lenders frequently remind buyers to maintain financial consistency throughout the transaction.

Escrow Helps Ensure Proper Title Transfer

Another major escrow responsibility involves coordinating title work. Before closing, title professionals investigate the property’s ownership history to identify liens, legal claims, unpaid taxes, or ownership disputes that could affect the buyer’s rights.

Escrow helps ensure that title issues get resolved before ownership transfers. That process protects buyers from inheriting unresolved legal or financial problems attached to the property.

A Smooth Escrow Starts With Preparation

A Smooth Escrow Starts With Preparation

The strongest real estate transactions usually begin with preparation long before escrow officially opens. Buyers who understand the financing process, secure full pre-approval, organize financial documentation, and communicate proactively with their lender often experience fewer delays and complications.

At the same time, experienced escrow professionals help guide transactions through each stage while protecting all parties involved. When financing, escrow coordination, and communication all work together effectively, buyers and sellers can move toward closing with far greater confidence.

About Exact Escrow in La Verne, California

Exact Escrow is your trusted partner for professional escrow services in Southern California. Based in La Verne, we bring decades of expertise to manage your transactions efficiently. Whether you’re buying, selling, or refinancing, our team is committed to providing reliable, detail-oriented support. Contact Exact Escrow for smooth, stress-free escrow services tailored to your needs.